Corporation

Corporate E-Kit

Perfect for the business owner who wants to form a Delaware corporation and wants everything handled digitally! You’ll receive your package via email.

Regular price

$189.00

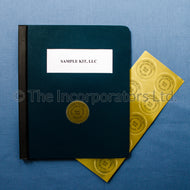

EZ Corporate Snap Kit

All of the advantages of a corporate minute book in a sleek and professional portfolio.

Regular price

$250.00

Corporate Executive E-Kit

Upgraded electronic package including gold 3-D company seal and electronic signature lines on stock certificates, on screen issuing of stock certificates, and a corporate name label document.

Regular price

$275.00

Executive Corporate Package

This package is for the business owner who wants to start a Delaware corporation and wants a professional, corporate minute book with all the accessories.

Regular price

$340.00